CBRE MarketView: Construction Investment Rebounds In Q2

CBRE Cambodia’s MarketView for the second quarter of this year (published below) shows some promising figures from the residential, office, retail and industrial sectors in Phnom Penh.

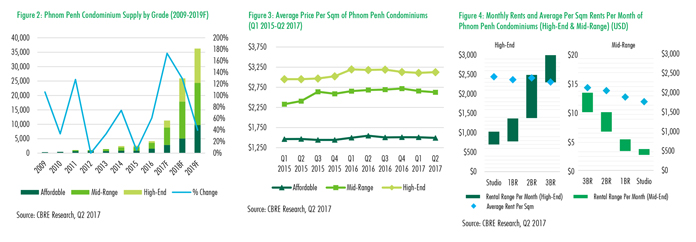

The average price of high-end condominiums in Phnom Penh has gone up to $3,126 per square metre in the second quarter of 2017, while the rent for prime condominiums has increased to $15.9 per square metre.

Highlights

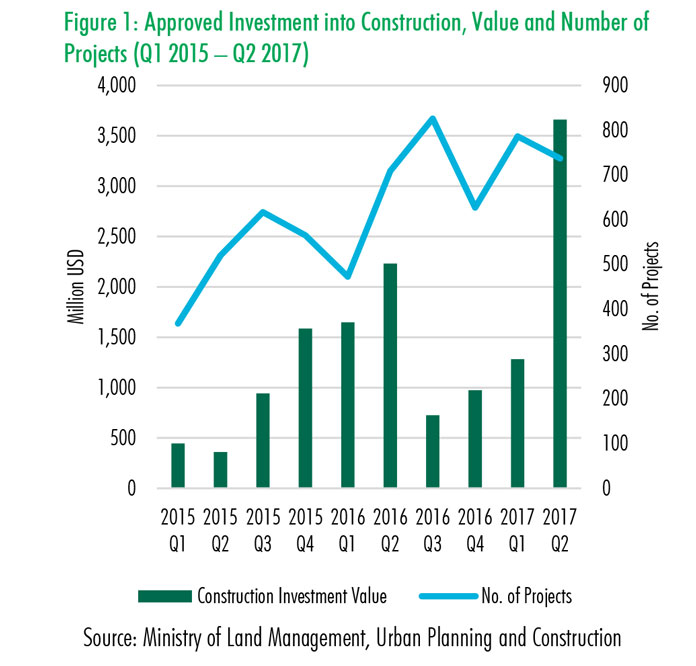

The value of approved investment into the construction sector saw a 64% increase year on year, totalling US$3.66 billion across 737 approved projects nationwide during Q2 2017. Only one condominium project was launched, the development is located on Chhroy Changvar peninsular and comprises 283 units. Sale prices and rents for condominiums were broadly stable in Q2, as they were during Q1 2017. By the close of Q2, overall office occupancy saw a marginal increase of 1.25 percentage points compared to the previous quarter. Average quoting rents for office space fell by 0.5% quarter-on-quarter, while quoting rents for prime retail witnessed a marginal increase over the same period.

Overview

During the course of Q2 this year, the value of approved investment into construction projects nationwide soared 64% year-on-year, and triple the value recorded in the previous quarter. A total of 737 projects gained approval, with a combined value of US$3.66 billion and comprising a total construction area of 5.2 million square meters. Of the 737 projects approved, most were residential and commercial projects, whilst 23 were in the industrial sector. No noticeable changes in rents for industrial properties were witnessed, despite notable increases in demand from Asian investors. During the second quarter, 1,911 condominium units were completed in Phnom Penh, pushing total supply to 6,109 units.

However, the number of new launches continues along a slow trajectory with only one project being announced in Q2. Condominium prices were broadly stable, though an approximate of 1% decrease was seen within the affordable and midrange segments. In the face of new supply, rents stood up well in the condominium sector, remaining stable across the quarter. Hongkong Land’s project ‘Exchange Square’ was completed and has delivered a total of 18,000 sqm Grade A office space and 8,000 sqm of retail.

In the wake of new office supply, overall occupancy rose by 1.25 percentage points across this quarter. However, average rents for Grade B offices fell by 1.4% quarter-on-quarter. Prime retail rents witnessed a slight increase in this quarter, with prime shopping malls and prime high streets accelerating by 1.6% and 4.5%, respectively.

Phnom Penh Condominiums

Condominium supply is still low at this stage with total supply of having expanded by 1,911 units to reach 6,109 units by the end of the second quarter of 2017, an increase of 46% from the previous quarter and approximately double the supply seen during the corresponding period last year.

Only one condominium project was launched offplan over the course of the second quarter. The project which is located on Chroy Changvar peninsular has added 283 units to the supply pipeline. Overall, average quoting sale prices were broadly stable during the second quarter compared to Q1 2017. An approximate 1% decrease in prices was witnessed within the affordable and mid-range segments, predominantly due to recently launched projects setting lower prices to target local buyers. It is worth noting that sales during the last two quarters have been slowing.

Whilst there has been little fluctuation in quoting sales prices for condominiums, some developers have started to employ increasingly commercial marketing strategies, including discounts on quoting sales prices of between 2% and 10%. Prime condominium rents were broadly stable in Q2, compared to those in Q1; however, rents are likely to face downward pressure as more stock completes over the course of the next 18 months.

Average rents of high-end condominiums in prime locations were recorded at circa $16 per square meter per month, whilst those in the mid-end segment in prime locations stood at $13 per square meter. Affordable condominiums achieved rents in the region of US$10 per square meter. Monthly rents for prime 1 bedroom units achieved between US$800 and US$1,500 per month, whilst prime 2 bedroom condominiums rented at between US$1,400 and US$2,500 per month.

Phnom Penh Office

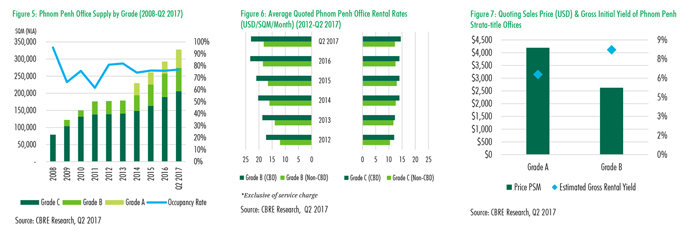

Exchange Square, the second Grade-A office in Phnom Penh, was completed and added 18,000 sqm of office space to total supply figures, representing an increase of 5.8% in total supply for Q2 compared to the previous quarter.

By the end of Q2, the overall occupancy rate recorded a marginal increase of 1.25 percentage points compared to previous quarter, indicating that demand is presently keeping pace with new supply. When the whole market is assessed, average rents witnessed a marginal decrease of 0.5% across the second quarter of 2017, compared to the previous quarter.

Average quoting rents for Grade B offices fell by 1.4% quarter-on-quarter, primarily the result of some offices buildings reducing their rents to compete for occupancy with newly completed Grade-C buildings. Grade B offices in prime positions maintained their rents across the quarter, indicating that it is within the non-CBD Grade B sector that competition for tenants is most keen. Quoting rents for Grade-A space remained stable at approximately US$28 per square meter, exclusive of service charge.

During Q2 2017, average quoting prices for strata-title offices stood at approximately $3,360 per square meter and ranged between $2,376 and $4,730 per square meter. Average quoting prices for Grade A offices were approximately $4,150 per square meter, whilst quoting prices for Grade B offices averaged $2,625 per square meter. CBRE estimate the Gross Initial Yield for Grade A and Grade B strata-title offices to be 6.3% and 8.2%, respectively.

Phnom Penh Retail

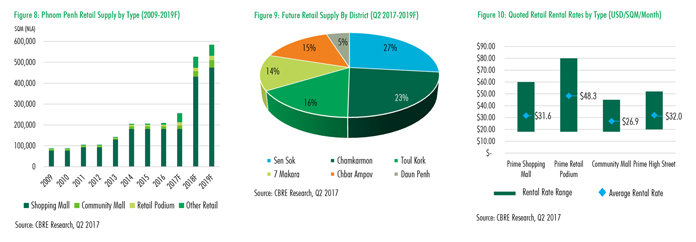

In addition to office space, Exchange Square delivered circa 8,000 square meters of net space into the capital’s retail supply over the course of Q2. The retail podium is home to a number of retail brands including Lucky Premium Supermarket, Pandora, Hard Rock Café, Legend Cinema and Starbucks.

It is worth noting that both local and regional retail operators are considering the grocery sector in Cambodia and Phnom Penh specifically. AEON opened its first premium stand-alone supermarket under the brand of AEON Maxvalu and has plans to expand to 30 stores across Phnom Penh and surrounding provinces, in addition to delivering its second mall which is slated to open in Q2 2018. Makro is currently on course to open its first outlet in Sen Sok District by the end of 2017.

As of Q2 2017, the majority of underconstruction retail projects are located within secondary districts, which is a trend set to diversify Phnom Penh’s retail landscape whilst also supporting the city’s urban expansion and population growth outside central districts. It is worth noting that Sen Sok accounts for 27% of future retail supply.

Further future retail supply located in the districts of Chbar Ampov and Mean Chey is largely in support of large residential-led developments. Prime retail rents saw a slight increase across the second quarter. As of Q2 2017, average rents within prime shopping malls were quoted at $31.6 per square meter per month, whilst community malls quoted an average of $26.9 per square meter. Average quoting rents for prime high-street units increased strongly, up 4.5% quarter-on-quarter to $32.0 per square meter, with top quoting rents in highstreet positions standing at $52 per square meter per month.

Phnom Penh Industrial

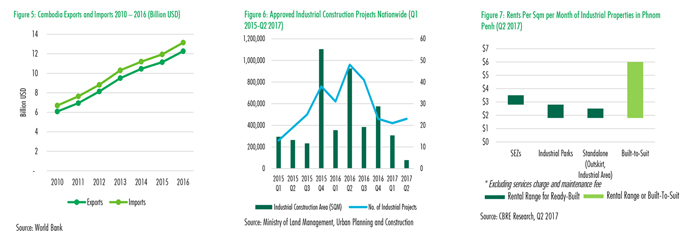

Following a decrease in 2016, exports to the US, a major export market for the Kingdom’s goods, saw an increase of 4.5% year-on-year to $1.36 billion during the first six month of 2017. In contrast, growth in exports to Japan slowed during H1 2017, totaling US$591 million, up by 4.5% year-on-year.

The ADB project that Cambodia’s exports will accelerate by 11%, which is higher than the 9% growth in imports expected for 2017. A total of 44 industrial projects were approved in the first six months of 2017, due to deliver a total of circa 385,000 sqm of industrial space, particularly in the forms of warehouses and factories. Although the figure for Q2 is dramatically less if compared to the same period last year or the previous quarter, CBRE is aware that demand for ready-built industrial premises has increased significantly, particularly in Phnom Penh, compared to the same period last year. Early this year, the ADB projected that growth in the industrial sector will be 10.8% in 2017.

The majority of demand for industrial properties in Phnom Penh is for space between 1,000 and 20,000 sqm with a particular concentration of demand in the range of 1,000 - 2,000 sqm. In the second quarter, no significant increases in rents were identified. The highest rents for ready-built factories were found within SEZs where rents reach $3.5 per sqm per month, a result of the demand for well established infrastructure available at SEZs. The lowest rents for ready-built factories were found within predominantly industrial locations on the city’s fringe, where quoting rents are $1.8 per sqm. Rents for built-to-suit space range between $1.8 per sqm per month for a warehouse or factory of minimal specification to $6 per sqm for space of international quality or for specialist uses.

To learn more about CBRE Research, or to access additional research reports, please visit the Global Research Gateway at www.cbre.com/researchgateway.